Federal Issues Committee :

The on-line links to the following articles can be found in the "issues archive" of our

Federal Issues Committee website [ http://www.indeedfree.com/fic/issues/archive.html ]

Today's Items -

http://en.wikipedia.org/wiki/United_States_budget_process

United States budget process

(excerpted from Wikipedia - pwc)

The process of creating the budget for the United States Government is known as the budget process. The framework used by Congress to formulate the budget was established by the Budget and Accounting Act of 1921,[1] the Congressional Budget and Impoundment Control Act of 1974,[2] and by other budget legislation. … Prior to 1974, Congress had no formal process for establishing a coherent budget. …

Overview of the budget process

The President, according to the Budget and Accounting Act of 1921, must submit a budget to Congress each year. … The President's budget contains detailed information on spending and revenue proposals, along with policy proposals and initiatives with significant budgetary implications.

Each year in March, the Congressional Budget Office (CBO) publishes an analysis of the President's budget proposals … CBO computes a current law baseline projection that is intended to estimate what federal spending and revenues would be in the absence of new legislation for the current fiscal year and for the coming 10 fiscal years.

The House and Senate Budget Committees begin consideration of President's budget proposals in February and March. Other committees with budgetary responsibilities submit requests and estimates to the Budget committees during this time. The Budget committees each submit a budget resolution by April 1. The House and Senate each consider those budget resolutions and are expected to pass them, possibly with amendments, by April 15. Budget resolutions specify funding levels for appropriations committees and subcommittees.

Appropriations committees, starting with allocations in the budget resolution, put together appropriations bills, which may be considered in the House after May 15. Once appropriations committees pass their bills, they are considered by the House and Senate. A conference committee is typically required to resolve differences between House and Senate bills. Once a conference bill has passed both chambers of Congress, it is sent to the President, who may sign the bill or veto. If he signs, the bill becomes law. Otherwise, Congress must pass another bill to avoid a shutdown of at least part of the federal government.

In recent years, Congress has not passed all of the appropriations bills before the start of the fiscal year. Congress has then enacted continuing resolutions, that provide for the temporary funding of government operations.

The President's budget request

Congressional consideration of the federal budget begins once the President of the United States submits a budget request, which is formulated over a period of months with the assistance of the Office of Management and Budget, the largest office within the Executive Office of the President. The budget request includes funding requests for all federal executive departments and independent agencies.

The President submits the budget request each year to Congress for the following fiscal year, as required by the Budget and Accounting Act of 1921. Current law [4] requires the President to submit a budget no earlier than the first Monday in January, and no later than the first Monday in February. Typically, Presidents submit budgets on the first Monday in February.

The President's budget request constitutes an extensive proposal of the administration's intended spending and revenue plans for the following fiscal year. The budget proposal includes volumes of supporting information intended to persuade Congress of the necessity and value of the budget provisions. In addition, each federal executive department and independent agency provides additional detail and supporting documentation to Congress on its own funding requests.

Budget resolution

The next step is the drafting of a budget resolution. The United States House Committee on the Budget and the United States Senate Committee on the Budget are responsible for drafting budget resolutions. Following the traditional calendar, by early April both committees finalize their drafts and submit it to their respective floors for consideration and adoption.

A budget resolution, which is one form of a concurrent resolution, binds Congress, but is not a law, and so does not require the President's signature. The budget resolution serves as a blueprint for the actual appropriation process, and provides Congress with some control over the appropriations process. No new spending authority, however, is provided until appropriation bills are enacted.

Once both houses pass the resolution, selected Representatives and Senators negotiate a conference report to reconcile differences between the House and the Senate versions. The conference report, in order to become binding, must be approved by both the House and Senate.

Fiscal year

The federal government's fiscal year currently begins on October 1 and ends on September 30 of the next calendar year. The fiscal year corresponds to the calendar year in which it ends; thus, fiscal year 2009 would begin on October 1, 2008 and end September 30, 2009. The federal fiscal year's starting date was shifted from July 1 to October 1 in 1976. The period between the end of FY1976 and the start of FY1977 was called the Transition Quarter. An earlier shift in the U.S. government's fiscal year was made in the 1850s.

Structure of the budget

[ section skipped - pwc]Discretionary vs. mandatory spending

Each function within the budget may include "budget authority" and "outlays" that fall within the broad categories of discretionary spending or direct spending.

Discretionary spending

Discretionary spending requires an annual appropriation bill, which is a piece of legislation. Discretionary spending is typically set by the House and Senate Appropriations Committees and their various subcommittees. Since the spending is typically for a fixed period (usually a year), it is said to be under the discretion of the Congress. Some appropriations last for more than one year (see Appropriation bill for details). In particular, multi-year appropriations are often used for housing programs and military procurement programs.

There are currently 12 appropriation bills that must be passed each fiscal year in order for continued discretionary spending to occur. The subject of each appropriations bill corresponds to the jurisdiction of the respective House and Senate appropriation subcommittees:

|

Agriculture |

Energy and Water |

Interior and Environment |

Military Construction and Veterans Affairs |

|

Commerce,Justice and Science |

Financial Services |

Labor, Health and Education |

State and Foreign Operations |

|

Defense |

Homeland Security |

Legislative Branch |

Transportation, Housing and Urban Development |

A continuing resolution is often passed if an appropriations bill has not been signed into law by the end of the fiscal year.

Mandatory spending

Direct spending, also known as mandatory spending, refers to spending enacted by law, but not dependent on an annual or periodic appropriation bill. Most mandatory spending consists of entitlement programs such as Social Security benefits, Medicare, and Medicaid. These programs are called "entitlements" because individuals satisfying given eligibility requirements set by past legislation are entitled to Federal government benefits or services. Many other expenses, such as salaries of Federal judges, are mandatory, but account for a relatively small share of federal spending. The Congressional Budget Office (CBO) estimates costs of mandatory spending programs on a regular basis.

Congress can affect spending on entitlement programs by changing eligibility requirements or the structure of programs. Certain entitlement programs, because the language authorizing them are included in appropriation bills, are termed "appropriated entitlements." This is a convention rather than a substantive distinction, since the programs, such as Food Stamps, would continue to be funded even were the appropriation bill to be vetoed or otherwise not enacted.

Authorization and appropriations

In general, funds for Federal Government programs must be authorized by an "authorizing committee" through enactment of legislation. Then, through subsequent acts by Congress, budget authority is then appropriated by the Appropriations Committee of the House. In principle, committees with jurisdiction to authorize programs make policy decisions, while the Appropriations Committees decide on funding levels, limited to a program's authorized funding level, though the amount may be any amount less than the limit.

In practice, the separation between policy making and funding, and the division between appropriations and authorization activities are imperfect. Authorizations for many programs have long lapsed, yet still receive appropriated amounts. Other programs that are authorized receive no funds at all. In addition, policy language—that is legislative text changing permanent law—is included in appropriation measures.

[1] Budget and Accounting Act of 1921http://frwebgate4.access.gpo.gov/cgi-bin/waisgate.cgi?WAISdocID=978089188734+0+0+0&WAISaction=retrieve

[2] Budget and Impoundment Control Act of 1974

http://frwebgate5.access.gpo.gov/cgi-bin/waisgate.cgi?WAISdocID=978741125627+0+0+0&WAISaction=retrieve

[4] 31 U.S.C. 1105(a)

http://www4.law.cornell.edu/uscode/uscode31/usc_sec_31_00001105----000-.html

Wikipedia

http://en.wikipedia.org/wiki/Baseline_%28budgeting%29Baseline (budgeting)

Baseline budgeting is a method of developing a budget which uses existing spending levels as the basis for establishing future funding requirements. The concept assumes that the organization is generally headed in the right direction and only minor changes in spending levels will be required. The baseline is normally enhanced by adding adjustment factors based on issues such as inflation, new programs, and anticipated changes to existing programs.

The genesis of baseline budget projections can be found in the Congressional Budget Act of 1974. That act required the Office of Management and Budget (OMB) to prepare projections of federal spending for the upcoming fiscal year based on a continuation of the existing level of governmental services. It also required the newly established Congressional Budget Office to prepare five-year projections of budget authority, outlays, revenues, and the surplus or deficit. OMB published its initial current-services budget projections in November 1974, and CBO's five-year projections first appeared in January 1976. Today's baseline budget projections are very much like those prepared more than two decades ago, although they now span 10 years instead of five.

The Budget Act was silent on whether to adjust estimates of discretionary appropriations for anticipated changes in inflation. Until 1980, OMB's projections excluded inflation adjustments for discretionary programs. CBO's projections, however, assumed that appropriations would keep pace with inflation, although CBO has also published projections without these so-called discretionary inflation adjustments.

CBO's budget projections took on added importance in 1980 and 1981, when they served as the baseline for computing spending reductions to be achieved in the budget reconciliation process. The reconciliation instructions contained in the fiscal year 1982 budget resolution (the so-called Gramm-Latta budget) required House and Senate committees to reduce outlays by a total of $36 billion below baseline levels, but each committee could determine how those savings were to be achieved. The CBO baseline has been used in every year since 1981 for developing budget resolutions and measuring compliance with reconciliation instructions.

The Deficit Control Act of 1985 provided the first legal definition of baseline. For the most part, the act defined the baseline in conformity with previous usage. If appropriations had not been enacted for the upcoming fiscal year, the baseline was to assume the previous year's level without any adjustment for inflation. In 1987, however, the Congress amended the definition of the baseline so that discretionary appropriations would be adjusted to keep pace with inflation. Other technical changes to the definition of the baseline were enacted in 1990, 1993, and 1997.

Baseline budget projections increasingly became the subject of political debate and controversy during the late 1980s and early 1990s, and more recently during the 2011 debt limit debate. Some critics contend that baseline projections create a bias in favor of spending by assuming that federal spending keeps pace with inflation and other factors driving the growth of entitlement programs. Changes that merely slow the growth of federal spending programs have often been described as cuts in spending, when in reality they are actually reductions in the rate of spending growth.

There have been attempts to eliminate the baseline budget concept and replace it with zero based budgeting, which is the opposite of baseline budgeting. Zero based budgeting requires that all spending must be re-justified each year or it will be eliminated from the budget regardless of previous spending levels.

According to the Government Accountability Office, a Baseline is as follows:

Baseline

"An estimate of spending, revenue, the deficit or surplus, and the public debt expected during a fiscal year under current laws and current policy. The baseline is a benchmark for measuring the budgetary effects of proposed changes in revenues and spending. It assumes that receipts and mandatory spending will continue or expire in the future as required by law and that the future funding for discretionary programs will equal the most recently enacted appropriation, adjusted for inflation. Under the Budget Enforcement Act (BEA), which will expire at the end of fiscal year 2006 [sic], the baseline is defined as the projection of current-year levels of new budget authority, outlays, revenues, and the surplus or deficit into the budget year and outyears based on laws enacted through the applicable date.

CBO Baseline

Projected levels of governmental receipts (revenues), budget authority, and outlays for the budget year and subsequent fiscal years, assuming generally that current policies remain the same, except as directed by law. The baseline is described in the Congressional Budget Office’s (CBO) annual report for the House and Senate Budget Committees, The Budget and Economic Outlook, which is published in January. The baseline, by law, includes projections for 5 years [sic], but at the request of the Budget Committees, CBO has provided such projections for 10 years. In most years the CBO baseline is revised in conjunction with CBO’s analysis of the President’s budget, which is usually issued in March, and again during the summer. The "March" baseline is the benchmark for measuring the budgetary effects of proposed legislation under consideration by Congress."

http://www.speaker.gov/UploadedFiles/3-7-31-11-Debt-Framework-Boehner.pdf

SPEAKER JOHN BOEHNER Updated: July 31, 10:35pm EST

TWO-STEP APPROACH TO HOLD PRESIDENT OBAMA ACCOUNTABLE

Emerging framework has three main features:

(1) cuts government spending more than it increases the debt limit;

(2) implements spending caps to restrain future spending;

(3) advances the cause of a Balanced Budget Amendment

Framework accomplishes this without tax hikes, which would destroy jobs, while preventing a job-killing national default.

NO TAX HIKES

Same as House-passed bill, the framework includes no tax hikes.

Under the framework, the Joint Committee of Congress will work off a current-law baseline, as required by the 1974 Budget Act, effectively making it impossible for Joint Committee to increase taxes.

CUTS THAT EXCEED THE DEBT HIKE

Same as House-passed bill, framework includes spending cuts that exceed the amount of the increased debt authority granted to POTUS.

Would cut & cap discretionary spending immediately, saving $917B over 10 years (certified by CBO) & raise the debt ceiling by less – $900B – to approximately February.

Before debt ceiling can be raised, Congress and the president must enact

spending cuts of a larger amount first.

CAPS TO CONTROL FUTURE SPENDING

As in House-passed bill, framework imposes spending caps that would set clear limits on future spending & serve as barrier against gov’t expansion while economy grows.

Failure to remain below these caps triggers automatic across-the-board cuts ("sequestration"). Same mechanism used in 1997 Balanced Budget Agreement.

BALANCED BUDGET AMENDMENT

Same as House-passed bill, framework requires both House & Senate to vote on a BBA after Oct. 1, 2011 but before the end of year.

Similar to House-passed bill, framework authorizes POTUS to request second tranche of debt limit increase of $1.5T if:

Joint Committee cuts spending by greater amount than the requested debt limit hike,

OR

A Balanced Budget Amendment is sent to the states.

Creates incentive for previous opponents of a BBA to now support it.

ENTITLEMENT REFORMS & SAVINGS

Same as House-passed bill, framework creates a 12-member Joint Committee required to report legislation by November 23, 2011 that would produce a proposal to reduce the deficit by at least $1.5T over 10 years.

Each chamber would consider Joint Committee proposal on an up-or-down basis without any amendments by December 23, 2011.

If Joint Committee’s proposal is enacted OR if a Balanced Budget Amendment is sent to the states, POTUS would be authorized to request a debt limit increase of $1.5T.

ENTITLEMENT REFORMS & SAVINGS

Sets up a new sequestration process to cut spending across-the-board – and ensure that any debt limit increase is met with greater spending cuts – IF Joint Committee fails to achieve at least $1.2T in deficit reduction.

If this happens, POTUS may request up to $1.2T for a debt limit increase, and if granted, then across-the-board spending cuts would result that would equal the difference between $1.2T and the deficit reduction enacted as a result of Joint Committee.

Across-the-board spending cuts would apply to FYs 2013-2021, and apply to both mandatory & discretionary programs.

Total reductions would be equally split between defense and non-defense programs. Across-the-board cuts would also apply to Medicare. Other programs, including Social Security, Medicaid, veterans, and civil & military pay, would be exempt.

Sequestration process is designed to guarantee that Congress acts on the Joint Committee’s legislation

to cut spending.

( excerpted from the American Thinker

- pwc) http://www.americanthinker.com/blog/2011/08/hostage-taking_butchering_lunacy.htmlHostage-taking, Butchering, Lunacy

by Randall Hoven August 1, 2011|

The new debt deal "would cut & cap discretionary spending immediately, saving $917B over 10 years." House Speaker John Boehner's PowerPoint slides. |

|

"[A] nearly complete capitulation to the hostage-taking demands of Republican extremists... many are counting on future Congresses to undo its arbitrary butchering... a political environment laced with lunacy." The New York Times. |

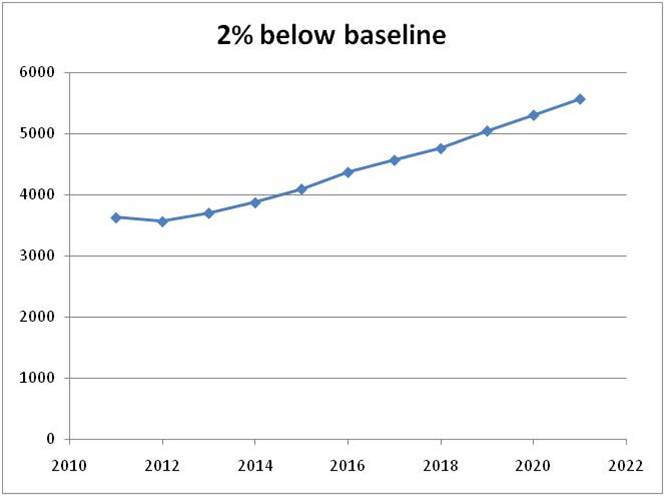

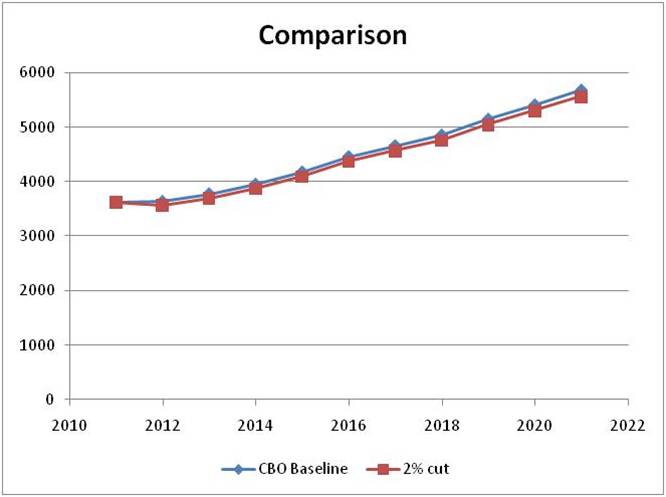

This is your federal budget. This is your federal budget with 2% "cuts."

Source: Congressional Budget Office, March 2011 baseline. Vertical axis is billions of dollars.

In case you find it difficult to see the difference, here are both budgets, cut and un-cut, on one chart.

- Total spending, 2012-21, in baseline: $45.769 trillion.

- Total spending, 2012-21, with "cuts": $44.854 trillion.

- Spending increase, 2011 to 2021, in baseline: 56.5% (4.6% per year, average).

- Spending increase, 2011 to 2021, with "cuts": 53.4% (4.4% per year, average).

Incidentally, the American Recovery and Reinvestment Act of 2009 (the "stimulus") will cost $814 B over 2009-2019, according to the CBO. The first $572 B of that came in just its first two years: 2009 and 2010. The above debt deal, assuming "cuts" are evenly spread over the next decade, will take seven years to simply undo two years of "stimulus" and a full decade to undo all of the "stimulus".

To summarize, by "cutting" $917 B from the CBO's baseline 10-year budget, spending will go up 4.4% per year on average instead of 4.6% per year, and will essentially undo about three years worth of "stimulus." That's what all the fuss was about.

-- Comparing some budgeting methods --

Baseline budgeting

(

http://en.wikipedia.org/wiki/Baseline_%28budgeting%29 )Baseline budgeting is a method of developing a budget which uses existing spending levels as the basis for establishing future funding requirements. The concept assumes that the organization is generally headed in the right direction and only minor changes in spending levels will be required. The baseline is normally enhanced by adding adjustment factors based on issues such as inflation, new programs, and anticipated changes to existing programs.

Zero-based budgeting

(

http://www.finweb.com/financial-planning/pros-and-cons-of-zero-based-budgeting.html )Zero-based budgeting is is a method wherein all the budgetary allocations for each department for the financial year are set at zero. The most important stipulation is that every financial-allocation-seeking department will justify their expenditure for the current year. The allocation of funds will be based only on the merits of their policy goals etc and not as per previous budgetary allotments. Mostly zero-based budgeting is encouraged for government budgets; but it can be applied to any private/public sector programs.

Incremental budgeting

( http://www.finweb.com/financial-planning/pros-and-cons-of-incremental-budgeting.html )

Incremental budgeting starts out with a budget from a previous period. The organization uses this previous budget as a basis for calculating the new budget. They take the old budget and add to or subtract from the totals to come up with a budget for the upcoming period.

(Rep. Connie Mack Press Office)

May 20, 2011H.R. 1848, the "One Percent Spending Reduction Act of 2011"

A Path to Balancing the Federal Budget

The Mack "One Percent Spending Reduction Act of 2011" (H.R. 1848) will achieve a balanced federal budget, beginning in 2019, by bringing federal spending down to average federal revenue over the past 30 years, which is 18% of gross domestic product (GDP).

KEY PROVISIONS:

One Percent Spending Reduction per Year: The Mack One Percent bill cuts total spending – mandatory and discretionary – by one percent each year for six consecutive fiscal years, beginning in fiscal year 2012.

- FY 2012 – $3.382 trillion*, less one percent => $3.348 trillion cap

- FY 2013 – $3.348 trillion, less one percent => $3.315 trillion cap

- FY 2014 – $3.315 trillion, less one percent => $3.282 trillion cap

- FY 2015 – $3.282 trillion, less one percent => $3.249 trillion cap

- FY 2016 – $3.249 trillion, less one percent => $3.216 trillion cap

- FY 2017 – $3.216 trillion, less one percent => $3.184 trillion cap

Overall Spending Cap in FY 2018: The bill sets an overall spending cap of 18 percent of GDP beginning in fiscal year 2018.

Enforcement of Spending Cuts: The one percent spending cuts would be achieved one of two ways: either 1) Congress and the President work together to enact program reforms and cut federal spending by one percent each year; or 2) If Congress and the President fail to do so, the bill triggers automatic, across-the-board spending cuts to ensure the one percent reduction is realized.

*Congressional Budget Office March 2011 Baseline for Total Outlays minus Net Interest

Presently the Mack Penny plan enjoys the support of more than 50 co-sponsors in the U.S House